Summary Investors last week continued to dump stocks and plough their money in safe haven assets.

KARACHI (Dunya News) – The stock market crashed in the early trading hours on Monday as confusion and uncertainty surrounded potential investors due to the decline in international oil prices by about 30 percent, the worst crash since the Gulf War in the 90s.

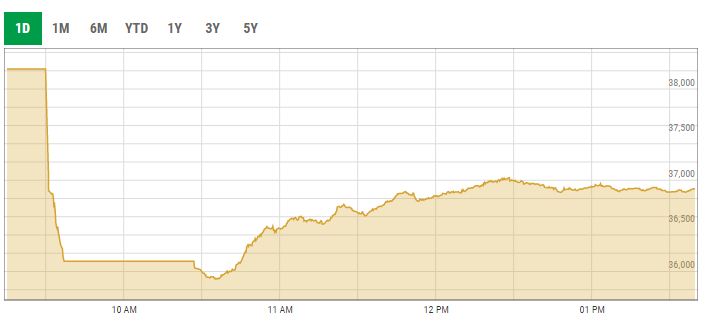

The Pakistan Stock Exchange’s (PSX) benchmark KSE 100-Share Index tumbled 2,291.69 points or 6pc around 10am, before recovering to 36,905.22 as of 1.39pm. The apex of the day remained 38,219.67 (the previous close) and 35,917.34, the lowest.

Moreover, trade activity was suspended around 9:45am after a rapid 5.83 per cent decline in share prices was witnessed and resumed around 10.30am.

Oil prices fell by as much as a third following Saudi Arabia’s move to start a price war after Russia balked at making the further steep output cuts proposed by OPEC to stabilise oil markets hit by worries over the global spread of the coronavirus.

Among other persisting factors, include the rout in global equities, the suspension of imports from China and the adverse affects on the Asian economy and sharper than expected downturn in world economies as the novel coronavirus outbreak continues to invade countries.

Investors last week continued to dump stocks and plough their money in safe haven assets, mainly gold.

According to experts, the stock market has been searching for a proper direction for healthy growth but several factors continue to dominate the sentiments of potential investors.

World stocks toppled by coronavirus shock, oil price crash

Global share markets tumbled on Monday as panicked investors fled headlong to bonds to hedge the economic trauma of the coronavirus, and oil plunged more than 30% after Saudi Arabia opened the taps in a price war with Russia.

Investors drove 30-year U.S. bond yields beneath 1% on bets the Federal Reserve would be forced to cut interest rates by at least 75 basis points at its March 18 meeting, despite only just having delivered an emergency easing.

The safe-haven yen surged across the board as emerging market currencies with exposure to oil, including the Russian rouble and Mexican peso, tumbled.

Saudi Arabia had stunned markets with plans to raise its production significantly after the collapse of OPEC’s supply cut agreement with Russia, a grab for market share reminiscent of a drive in 2014 that sent prices down by about two thirds.

The shock in oil was seismic as Brent crude LCOc1 futures slid $13.53 to $31.74 a barrel in chaotic trade, while U.S. crude CLc1 shed $13.45 to $27.83.

“Today’s price action puts at risk the fiscal health of the vast majority of sovereign producers and budget cuts and increased debt loads are now looming in the event of a prolonged period of low prices,” warned Helima Croft, head of global commodity strategy at RBC Capital Markets.

“For the most politically and economically fragile producer states, the reckoning could be severe.”

There were also worries that U.S. oil producers that had issued a lot of debt would be made uneconomic by the price drop.

Energy stocks took a beating and E-Mini futures for the S&P 500 ESc1 dived 4.89% to be limit down. EUROSTOXXX 50 futures STXEc1 fell 5.9% and FTSE futures FFIc1 6.8%.

Japan’s Nikkei fell 5.2% and Australia’s commodity-heavy market 6.4%.

MSCI’s broadest index of Asia-Pacific shares outside Japan lost 3.9% in its worst day since late 2015, while Shanghai blue chips dropped 2.8%.

“Wild is an understatement,” said Chris Brankin, Chief Executive at stockbroker TD Ameritrade Singapore.

“Not just us, but across the globe you would have every broker/dealer raising their margin requirements...trying to basically protect our clients from trying to leverage too much risk or guess where the bottom is.”

Not helping the mood was news North Korea had fired three projectiles off its eastern coast on Monday.

And Italy’s markets are sure to come under fire after the government ordered a lockdown of large parts of the north of the country, including the financial capital Milan.

The number of people infected with the coronavirus topped 107,000 across the world as the outbreak reached more countries and caused more economic carnage.

“After a week when the stockpiling of bonds, credit protection and toilet paper became a thing, let’s hope we start to see some more clarity on the reaction,” said Martin Whetton, head of bond & rates strategy at CBA.

“Dollar bloc central banks cut policy rates by 125 basis points, not as a way to stop a viral pandemic, but to stem a fear pandemic,” he added, while noting many had little scope to ease further.

BOND BUBBLE

A tectonic shift saw markets fully price in an easing of 75 basis points from the Fed on March 18, while a cut to near zero was now seen as likely by April.

The European Central Bank meets on Thursday and will be under intense pressure to act, but rates there are already deeply negative.

“The onus is falling, perhaps inevitably on the actions of governments to abandon budget surpluses and reinvigorate the demand side of the economy,” said Whetton.

Urgent action was clearly needed with data suggesting the global economy toppled into recession this quarter. Figures out from China over the weekend showed exports fell 17.2% in January-February, from a year earlier.

Analysts at BofA Global Research estimated the latest sell-off had seen $9 trillion in global equity value vaporised in nine days, while the average 10-year yield in the developed world hit 16 basis points, the lowest in 120 years.

“The clearest outcome of the exogenous COVID-19 shock is a collapse in bond yields, which once panic fades can induce huge rotation to ‘growth stocks’ and ‘bond proxies’ in equities,” they wrote in a client note.

Yields on 10-year U.S. Treasuries US10YT=RR plunged to a once-unthinkable 0.48%, having halved in just three sessions.

Yields on the 30-year long bond US30YT=RR dived 35 basis points on Friday alone, the largest daily drop since the 1987 crash, and slid under 1% on Monday to reach 0.96%.

The fall in yields and Fed rate expectations has pulled the rug out from under the dollar, sending it crashing to the largest weekly loss in four years =USD.

The dollar extended its slide in Asia to as far as 101.60 yen depths not seen since late 2016. It was last down 2.4% at 102.80 in wild trade.

The euro likewise shot to the highest in over 13 months at $1.1492, to be last at $1.1406.

Gold initially cleared $1,700 per ounce XAU= to a fresh seven-year peak, only to fall back to $1,669.93 amid talk some investors were having to sell to raise cash to cover margin calls in stocks.

Energy firms hammered

Jeffrey Halley, senior market analyst at OANDA, said: "Saudi Arabia seems intent on punishing Russia.

"Oil prices... will likely be capped over the next few months as coronavirus stalls economic growth, and Saudi Arabia opens the pumps and offers huge discounts on its crude grades."

Energy firms were slammed, with Hong Kong-listed CNOOC tumbling 16 percent and PetroChina down 10 percent, while in Tokyo, Inpex dived 13 percent and Woodside Petroleum in Sydney fell 17 percent.

"Plummeting oil prices and spreading coronavirus are fanning fears of downside risks to the global economy," said Takuya Kanda, at Gaitame.com Research Institute.

Foreign exchange markets were also extremely volatile, with traders snapping up the yen -- seen as a hedge against global instability -- and selling off the dollar owing to uncertainty over the coronavirus in the United States.

Marito Ueda, senior trader at FX Prime, told AFP: "Fears over the virus’s impact on the global economy and a plummet in US yields had investors seeking the safe-haven yen."

"It is essentially a flight from the dollar," he added.

The greenback fell below 103 yen, levels not seen since the third quarter of 2016.

Analysts warned of further gyrations as the outbreak shows no sign of abating, with more than 100,000 people infected in 99 countries.

Italy, which is now the hardest hit country outside China, has put a quarter of its population in lockdown, while sporting and public events around the world have been cancelled.

"You just don’t know which way things are going to go, it makes it very hard to price anything right now," said Sarah Hunter, chief economist for BIS Oxford Economics, on Bloomberg TV.

"We’re seeing that in the market with the wild oscillations that are coming through."

Key figures around 0410 GMT

Brent Crude: DOWN 29.9 percent at $36.05 per barrel

West Texas Intermediate: DOWN 30.9 percent at $28.52

Tokyo - Nikkei 225: DOWN 5.9 percent at 19,536.01

Hong Kong - Hang Seng: DOWN 3.5 percent at 25,230.55 (break)

Shanghai - Composite: DOWN 2.4 percent at 2,961.29 (break)

Gold: UP 1.7 percent at $1,702 per ounce

Dollar/yen: DOWN at 102.43 yen from 105.40 yen at 2200 GMT Friday

Euro/dollar: UP at $1.1401 from $1.1298

Pound/dollar: UP at $1.3105 from $1.3051

Euro/pound: UP at 87.00 pence from 86.58 pence

New York - Dow: DOWN 1.0 percent at 25,864.78 (close)

London - FTSE 100: DOWN 3.6 percent at 6,462.55 (close)